Hong Kong through the Looking Glass: A Series on Sustainable Planet, People, and Prosperity

Hong Kong housing prices decreased 70 percent over six years. Does that remind you of anything that happened recently in the U.S.?

In 1981 mortgage interest rates were around 13 percent and we bought our first house in a gritty Cambridge, Massachusetts neighborhood for about $80,000. Our neighbor Charlie (a.k.a. Charlie Bad Teeth for obvious reasons when he smiled) frequently bragged about the pistol he had in case of burglars. Across the street an upright claw-foot bathtub half buried in the front yard framed the Virgin Mary. Our “new” house had no bathroom sinks when we moved in and we found a milk bottle from the 1800’s in a wall cavity.

The lender required that we make a 20 percent down payment, around $16,000. In those days 20 percent down was the standard. It took hard work to accumulate that much money even with parents’ help. But we’d been planning ahead for a while and were frugal. Every paycheck we put away as much as we could. We didn’t use credit cards. We didn’t feel deprived of anything. (Well that’s not exactly true: on frigid New England winter nights when the temperature inside our apartment fell to around 50 degrees F because we didn’t want to exceed our heating oil budget we felt that some insulation in the walls would have been nice.) More importantly, because we had savings we never ever were living paycheck to paycheck.

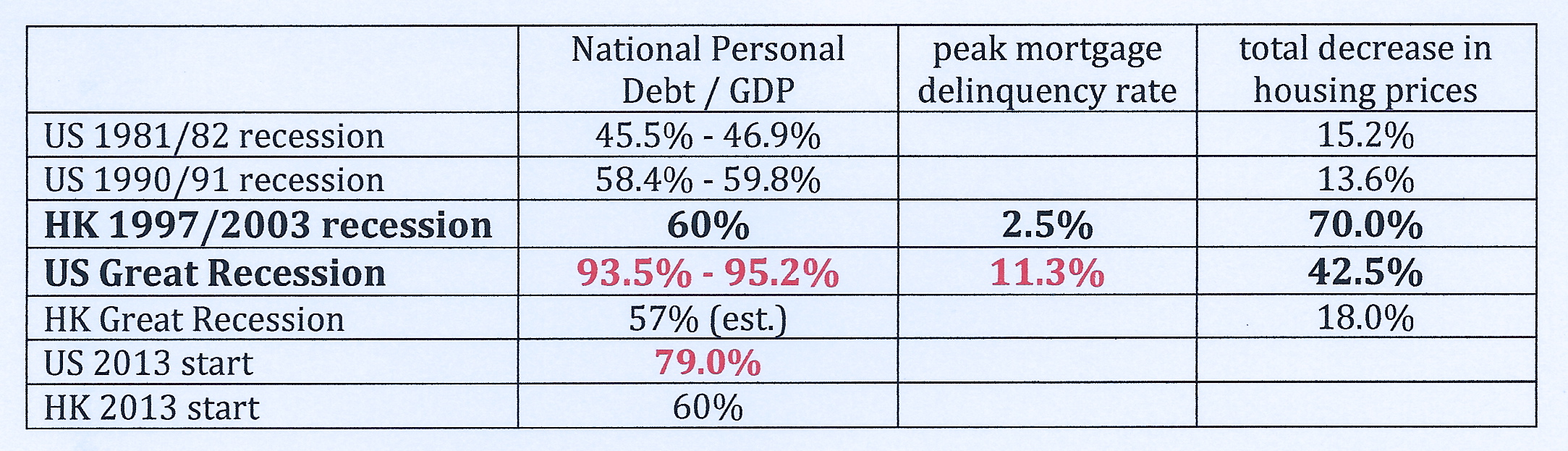

A lot changed in US mortgage lending and personal finance between 1981 and the first decade of the new millennium. Low and no down payment and other risky mortgages too freely given resulted in borrower defaults that ultimately led to the Great Recession and the too-big-to-fail-banks bailout. Although the US recession was officially over in mid-2009 the nation and especially Tucson still haven’t recovered. US average home prices did not stop falling until early 2012. At that point they were 42.5% below their 2006 highs. They are still about 34 percent lower than their highs. In Tucson values fell further and have further to climb back. During the housing market downturn US aggregate home mortgage delinquency rates reached 11.27 percent. Subprime mortgage delinquencies were as high as almost 30 percent.

Hong Kong on the other had a much shorter Great Recession. Although it was buffeted by external economic forces it avoided a downturn for almost a year longer than the U.S. and emerged about the same time. Housing prices fell about 18 percent and recovered all lost ground in less than a year. Ten years earlier a much worse Hong Kong housing crash occurred, again due to outside forces. The 1997 Asian financial crisis and significant emigration due to concerns about the switch from British to Chinese rule caused the price drop recounted at the beginning of this post. But even in the face of that huge 70 percent value decrease mortgage delinquency rates never exceeded 2.5 percent.

Why was there such a difference between U.S. and Hong Kong mortgage delinquency rates during their respective severe recessions? Maybe different attitudes toward borrowing have something to do with it.

Unlike the U.S., easy credit and even easily setting up a bank account do not seem to be the norm here. At least not at our bank. Establishing a checking account and then adding me to it was an arduous process requiring many documents, several trips to the bank, and multiple reviews and correction of many forms by many people. You’d think we wanted to take money from HSBC rather than give it to them.

Unlike the U.S., easy credit and even easily setting up a bank account do not seem to be the norm here. At least not at our bank. Establishing a checking account and then adding me to it was an arduous process requiring many documents, several trips to the bank, and multiple reviews and correction of many forms by many people. You’d think we wanted to take money from HSBC rather than give it to them.

The bank wouldn’t even allow us apply for a credit card account until at least one of us had a Hong Kong ID card. The ID card process takes at least 30 days after you arrive and you have to qualify as a Hong Kong resident which requires a visa for foreigners. Once we were actually allowed to apply we made the mistake of saying we each wanted a card. There was no way the bank could do that! How could we possibly think that I could get a credit card without being employed here? That got worked out once we realized that we needed to make it clear that we wanted only one Visa account, backed by my spouse’s salary, with two cards. But we had to think of that way around the problem ourselves. The bank didn’t suggest it.

Many retailers don’t accept credit cards, certainly not independent small retailers. Even the Apple Store won’t accept our HSBC Visa, although they will accept our debit card linked to the EPS network. At least they did think to tell us that EPS cards are okay–for the second purchase we made there. The first time they sent us to the nearest ATM. Racing the Planet, a local store with an international e-commerce web site, would accept my U.S. Visa but not my Hong Kong Visa. We had to go through an additional process to get HSBC approval for the use of their credit card for an online purchase.

Many retailers don’t accept credit cards, certainly not independent small retailers. Even the Apple Store won’t accept our HSBC Visa, although they will accept our debit card linked to the EPS network. At least they did think to tell us that EPS cards are okay–for the second purchase we made there. The first time they sent us to the nearest ATM. Racing the Planet, a local store with an international e-commerce web site, would accept my U.S. Visa but not my Hong Kong Visa. We had to go through an additional process to get HSBC approval for the use of their credit card for an online purchase.

People here tend to use credit cards a lot less and cash a lot more than in the U.S.

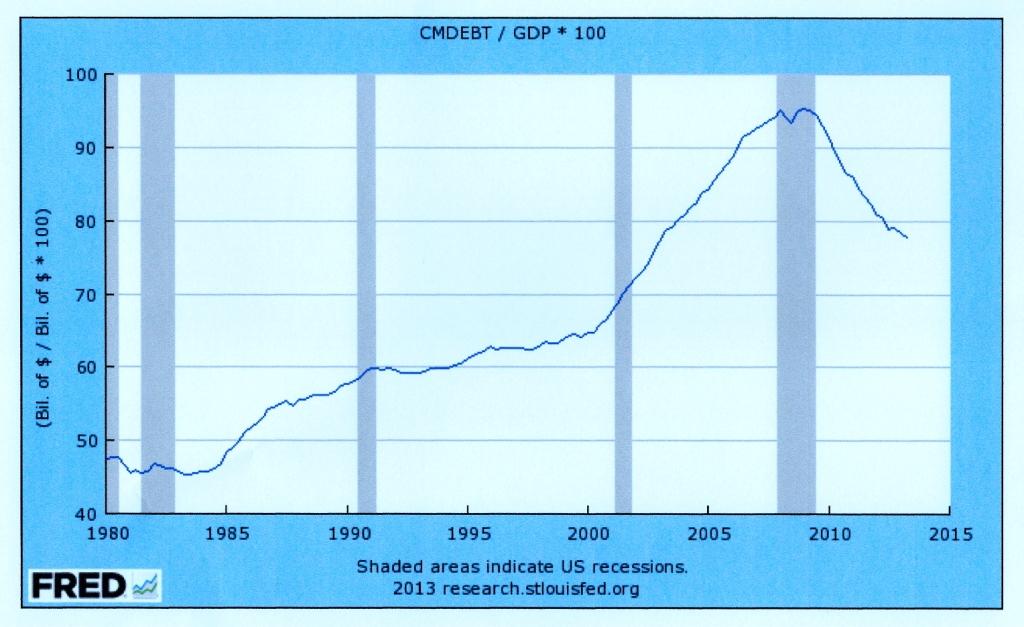

In Hong Kong during their early 2000 real estate market crash the National Personal Debt (note 1) to Gross Domestic Product (NPD/GDP) ratio was at a then record high for Hong Kong of about 60 percent. In 1981 when we had to make a 20 percent down payment to buy a house the NPD/GDP in the U.S. was below 50 percent. During the U.S.’s 1990/91 recession when housing prices fell 13.6 percent NPD/GDP was about 60 percent. But it shot up to almost 90 percent in the US in 2006 prior to the Great Recession and peaked at 95 percent in 2008 and 2009. It’s no wonder that huge numbers of mortgage delinquencies and defaults ignited the Recession and then accelerated and added fuel to the fire. When individuals borrow too much it’s hard for them to handle even small financial setbacks.

By the beginning of 2013 U.S. NPD/GDP had fallen but still was at a historically high level of 79 percent while Hong Kong’s was at 60 percent. In February 2013 because of concerns about a possible housing market bubble the Hong Kong Monetary Authority proposed requiring mortgage down payments ranging from 30 percent to 50 percent depending on the size of the mortgage. In May the Hong Kong Legislative Council expressed their concerns about what they considered a worrisome amount of household debt. Obviously right now the U.S. isn’t experiencing a market bubble, but we still have the worry of historically high rates of household debt.

So when the National Association of Home Builders reports that they “scored an important victory for builders and home buyers… when regulators withdrew a proposed… standard that would have resulted in 20 percent down payments becoming the market standard,” I’m skeptical about the wisdom of that. Excessive personal borrowing resulting in excessive mortgage defaults got the US into the economic mess that it’s still in. Making it easier for us to repeat past mistakes isn’t the conservatism that NAHB claims to espouse out of the other side of its mouth. As the Great Recession showed excessive personal borrowing isn’t sustainable.

Maybe the U.S. can learn something from Hong Kong’s personal borrowing habits. But maybe not. We don’t seem to have learned from our own history.

Note 1: What I call National Personal Debt (NPD) is what the Hong Kong Monetary Authority calls Household Debt and the U.S. Federal Reserve calls Credit Market Debt (CMDebt). They don’t measure exactly the same thing but are similar.

This post does not try to address, even indirectly, the matter of U.S. government debt.